Something is happening in the snack aisle, and most people haven't really noticed yet. The colorful bags and flashy packaging are all still there. The familiar logos still beckon from eye-level shelves. Yet behind that facade of normalcy, some of America's most beloved munchies are quietly bleeding customers, sale by sale, quarter by quarter.

We're not talking about tiny niche products either. We're talking about snacks that shaped childhoods, powered road trips, and lived permanently in every office break room within memory. The sales data rolling in between 2024 and 2026 tells a story that snack giants would rather not broadcast loudly. Let's dive in.

1. Cheetos: The Orange Dust Icon Losing Its Grip

Cheetos were once basically unstoppable. For decades, that electric-orange puff was synonymous with carefree snacking. Yet the numbers are now telling a different, less satisfying story.

Frito-Lay North America, which makes Cheetos along with Doritos and Lay's, experienced a decline in organic revenue for both the full year 2024 and the fourth quarter, with full-year organic revenue decreasing by 0.5%, a significant drop from the 9% growth seen just a year earlier in 2023. That shift is more dramatic than it sounds for a category that had been on a hot streak.

The average price of a bag of chips in June 2024 hit $6.56, prompting Frito-Lay to finally acknowledge that the cost of a bag of Cheetos was becoming a real burden on consumers' wallets. After years of price hikes, including double-digit increases in 2022 and 2023, PepsiCo eventually announced price cuts of as much as 15% on some of its biggest snack brands including Cheetos, Doritos, Lay's, and Tostitos.

Health consciousness around artificial colorings, such as Yellow 6 used in Cheetos, has emerged as a recognized risk factor for the brand. The "Make America Healthy Again" regulatory wave under the current administration has put additional scrutiny on exactly these kinds of ingredients, making it harder for Cheetos to simply coast on nostalgia.

2. Doritos: Volume Declines Signal a Shift in Taste

Honestly, few snacks have the cultural footprint that Doritos built over the past five decades. Bold flavor, loud crunch, stained fingertips and all. Still, the volume numbers are not what they used to be.

PepsiCo, which owns Doritos as part of its Frito-Lay portfolio, saw snack volumes declining five quarters in a row, with a 2% dip in organic revenue in its North American foods division during Q1 2025. That kind of sustained downward trend doesn't just happen overnight.

The drop in volume is significant because salty snacks like Doritos have seen steeper price increases than many other grocery items. Since 2020, the price per ounce of salty snacks rose by 36%, outpacing the overall 21% increase in grocery store prices. Consumers are simply doing the math and walking away. As part of a broader restructuring deal reached in December 2025, PepsiCo committed to reducing its U.S. product lineup by nearly 20% by early 2026.

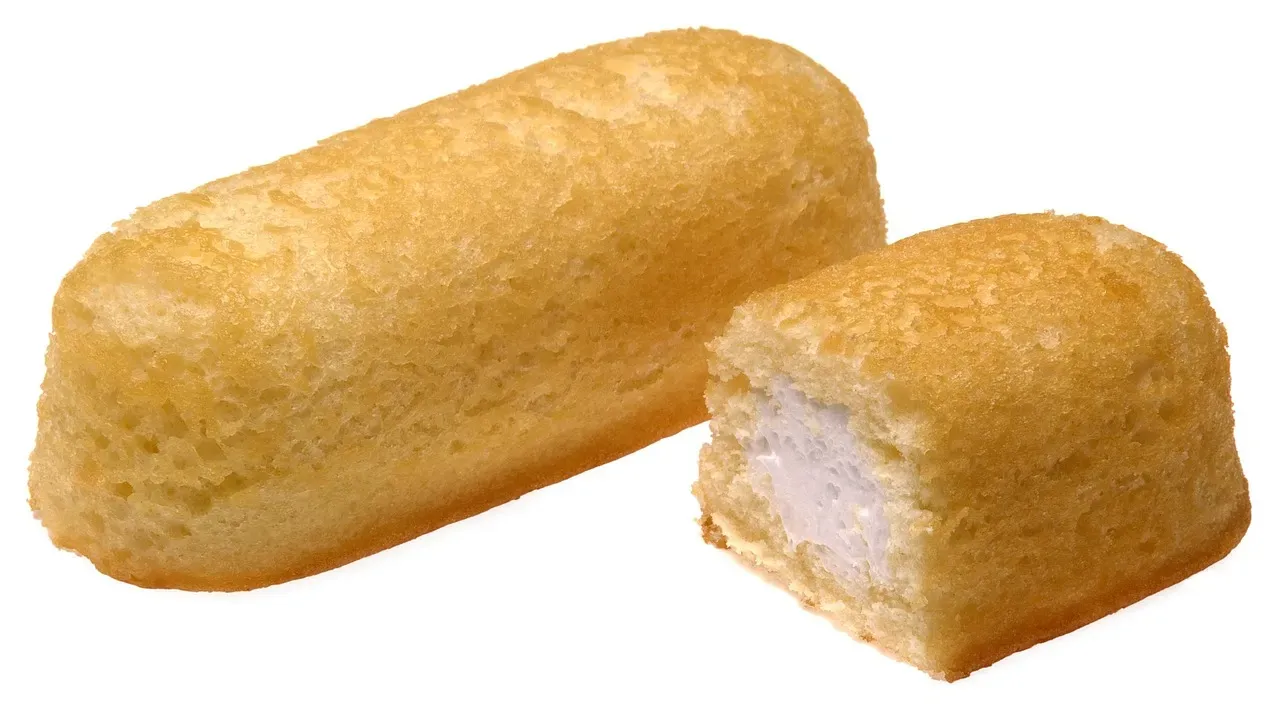

3. Twinkies and Hostess Sweet Baked Goods: A Financial Meltdown

Few snack stories in recent memory are as dramatic as what has happened to Twinkies and the broader Hostess product family. These golden sponge cakes practically define American junk food nostalgia. The business reality, though, is brutal.

Smucker's Q3 2025 results delivered the first serious blow, with the Sweet Baked Snacks segment posting an 8% sales decline. The company then dropped a $794 million goodwill impairment and wrote down another $208 million off the value of the Hostess brand trademark.

Less than three months later, Q4 results made that look almost mild. Sales for the segment dropped again, this time by a staggering 14%, followed by another $867 million in goodwill impairment. The Hostess fallout makes clear what many in the industry had suspected: sweet baked snacks are falling out of step with today's tastes, with classics like Twinkies and CupCakes losing ground as younger consumers chase protein, clean labels, and something new.

4. Chips Ahoy! Cookies: Mondelēz Feels the Pressure

Chips Ahoy! has been a lunchbox staple for generations. That navy-blue bag, the crunch, the chocolate chips. It feels like it should be timeless. The sales figures heading into 2025 suggest otherwise.

Mondelēz International, home to both Oreo and Chips Ahoy!, saw a 4.1% net revenue drop in North America, with its CEO citing a consumer shift toward grocery staples like meats and eggs. That kind of commentary from a CEO reveals just how deeply consumer priorities have been reshuffled.

According to the International Food Information Council's 2024 Food and Health Survey, roughly three out of four consumers are now actively trying to limit or avoid sugars, and demand for "better-for-you" snacks continues to rise in the U.S. Classic cookies loaded with sugar are sitting right in the crosshairs of that shift. The writing on the wall is hard to ignore.

5. Pork Rinds: A Steep and Sustained Drop

Pork rinds had a genuine moment a few years back. Keto diets turned them into an unlikely health darling. Protein, low carbs, satisfying crunch. For a while, it seemed like a category on the rise. That rise stalled hard.

The pork rind category's difficulties that started in 2022 continued into 2023 with dollar sales down 5.5%, unit sales down 10.2%, and volume sales down 10.3%. Those are not small fluctuations. Those are category-defining declines happening across every measurable metric simultaneously.

The category remains cautiously optimistic because pork rinds still fulfill a vital role in consumers' dietary routines, particularly with high-protein and low-carb snack seekers. It's hard to say for sure whether pork rinds can reclaim their brief spotlight moment, but right now the trajectory points stubbornly downward. Think of it as a one-hit-wonder still waiting for the follow-up album.

6. Standard Crackers: Dollar Growth Masking Real Volume Losses

Here's the thing about cracker sales data: at first glance, the headline numbers look deceptively healthy. Look a little closer, though, and the story changes fast.

Cracker sales topped $9.4 billion with a dollar sales increase of 7.2%, although unit sales actually dropped 3.3%. In plain English: people are paying more per box, but they're buying fewer boxes. That's not growth. That's inflation doing the accounting work for you.

At Campbell's, the CEO admitted that cookie and cracker sales didn't rebound as hoped, leading the firm to lower its 2025 sales forecast. The cracker category is in a strange middle ground right now. Not exactly collapsed, but quietly losing real consumers while brands celebrate dollar figures that are mostly inflated prices in disguise. Classic sleight of hand.

7. Popcorn: After a Blazing 2022, the Air Has Come Out

Popcorn had a genuinely spectacular run. In 2022, the category seemed invincible, with brands posting double-digit growth that felt almost impossible to sustain. Then came 2023, and the category returned to earth with a thud.

In 2023, after total popcorn sales had risen 13.1% in 2022 and seven out of the top 10 brands had boasted double-digit sales increases, the category flipped to just a 1.4% increase in dollar sales alongside a 4.3% decrease in unit sales. That's a swing most investors and analysts didn't see coming.

Softening sales are not because of a lack of flavor innovation, as popcorn producers have been actively competing in the broader snacking arena. Frito-Lay even closed its Liberty, New York PopCorners manufacturing plant in June 2025, laying off 287 workers. When a company closes a dedicated production facility, you know the volume decline is being taken very seriously indeed.

8. Traditional Potato Chips: Still Big, But Volumes Are Slipping

Potato chips remain the undisputed king of the salty snack world by sheer dollar size. However, even kings can feel the pressure from a population increasingly asking hard questions about what's in their bag.

The total potato chip category reached $8.6 billion in sales, a 7.7% increase from 2023, while unit sales saw a meaningful decline of 1.9%. Once again, the same pattern appears: prices rise, but actual units sold are dropping. The real consumer behavior is hidden underneath inflated price tags.

Federal Reserve data confirms the average price of potato chips in June 2024 was $6.56, nearly 30% higher than the $5.09 average during the pandemic period in June 2020. Faced with inflationary pressures and shrinking purchasing power, consumers began turning to more affordable private-label brands or cutting back on non-essential purchases like salty snacks altogether. Loyalty only stretches so far before the wallet wins the argument.

9. Sweet Baked Snack Cakes (Broader Category): A Generation Moving On

Beyond Twinkies specifically, the broader sweet baked snack cake category is facing a generation-defining reckoning. The kids who grew up putting these in lunchboxes are now reading nutrition labels like detectives.

J.M. Smucker, which owns Hostess Brands, reported a third-quarter 7% drop in sales of sweet baked snacks, and that was before the even steeper drops that followed. Regulators, emboldened by the "Make America Healthy Again" agenda, have put both more pressure and a bigger spotlight on processed foods, while the rise of GLP-1 drugs has meant some of food companies' key consumers have lost their appetite for sweet and salty snacks.

By April 2025, NielsenIQ consumer research found that nearly half of U.S. shoppers said they were buying fewer snacks, with the biggest decline in impulse buys, the kind of snacks that used to leap into carts without a second thought. Sweet snack cakes are the definition of an impulse purchase. When those disappear from the cart, an entire category feels it.

Leave a Reply